A net sheet is a document that lists the expenses paid for by you and your lender, as well as any gains/losses incurred on the sale of the property. It shows how much money you will receive from the sale to use towards paying off debts (e.g., mortgage payoff), closing costs, or reinvesting in another property.

This is also called “seller’s net” because it displays what amount of gain has been made during this particular transaction given all inputted data such as listing price and commissions paid out to agents involved with selling the house.

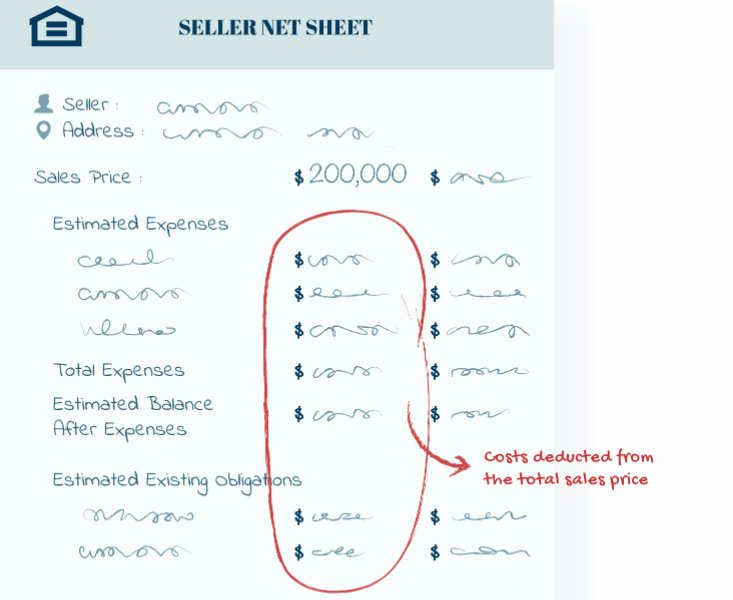

The typical seller’s net sheet includes columns that calculate: income; expense; taxes due at settlement date; funds available after settlement date for investment or debt reduction; and the difference between what was paid for sale (expenses) and the amount of money due at closing.

It matters because this is your chance to create financial stability in your life. Your real estate agent should be helping you get information about your lender’s requirements, as well as all expenses that will come up once you buy a home.

In addition, they need to help with calculating how much it’ll cost to pay back loans after interest rates are applied. This way you can plan ahead on how many hours/monthly salary it would take from now until when the payoff date comes around before considering the purchase.

It also means you can estimate the value of your new home, and whether or not the purchase is actually worth it in terms of time, energy, and finances.

Seller’s net sheets have been around for a long time and are a key part of the process for homebuyers. They can be tedious to fill out, but they’re worth it in order to understand what your true financial situation will be like after buying a house.

The first section on a Seller Net Sheet looks like “Listing Price: $100,000″. The number in parentheses indicates what was paid for the property when it was purchased – “$0” means that there were no costs associated with purchasing the house.

This section lists all the expenses related to selling a home, such as commissions paid to agents and brokers. If an agent sold your house for $135,000 with only listing fees of $500 (which is common), then they would take home about $133,500 after commission.

Individuals who are in charge of paying off a mortgage from their personal account will also see their payoff amount listed under “Mortgage Payoff:”.

One important thing I want you to note is that there can be different columns labeled “Adjustments/Deductions” because this form has been customized. For example, some people might find it helpful to list things like property taxes and capital gains tax on column C while others might prefer to list them under “Adjustments/Deductions.”

Here are the numbers that appear on the sheet:

- Estimated sales price. This is the price the seller expects to get for the house. The price depends on many factors, such as the condition of the house and location. A successful real estate agent should help you come up with the right estimated price.

- Listing price. Agent listing price is the amount that was paid for a property when it was originally purchased – $0 means there are no costs associated with buying this home. The seller’s net sheet also includes closing costs in this section to help you understand your total profit or loss on selling this particular house.

- The estimated cost of sale. This is a list of all costs associated with selling the property and includes closing fees, commissions paid to agents or brokers, real estate taxes (principal only), and capital gains tax due at settlement.

- Adjustments/deductions. Any adjustments from previous transactions may appear in this column. For example, if you had made improvements on your home that were not reflected in its value before it was sold, then those expenses would show up here as well as any capital gains tax owed by the seller prior to settlement. If there are no adjustments listed in this section then the line will be left blank.

- Mortgage loan payoff. This is the amount of money the seller owes on their mortgage before they receive any proceeds from the sale. The buyer will be responsible for paying this amount at settlement.

- Net proceeds. This is a number that shows you your total profit or loss based on how much you paid for the home and what it sold for. The final column labeled “NET” will show this information in dollars, but some people prefer to see it expressed as a percentage. A good rule of thumb is between 40-60%. Anything below 30% return would make me want to think twice about selling my house because I wouldn’t be making very much.

- The “net proceeds” section of a seller’s net sheet can be calculated by subtracting the mortgage payment ($0) and adjustments (such as insurance premiums or property taxes that are not included in escrow) from the estimated sales price. The result represents what you would receive after selling your home if these expenses were paid for upfront rather than being split between buyer and seller during closing. As this is just an estimate on how much money will eventually come to you after all costs have been covered by buyers and sellers alike, it does not reflect your final net proceeds.

- Attorney fees. This is a list of all costs associated with selling the property and includes closing fees, commissions paid to agents or brokers, real estate taxes (principal only), and capital gains tax due at settlement.

- Grantor’s Tax. This is the sum of all taxes, fees, and costs charged to a seller when they sell their property for more than its original cost basis.

- Transfer Tax. This depends on whether it will be going through county or city channels. Transfer tax is paid by sellers at settlement in order to record the sale from one owner’s name into another’s. The charge varies depending on which state you are buying or selling real estate in because each has different rules about how much transfer tax needs to be paid as well as what type of properties are exempt from transfer tax; some states may even have no transfer taxes whatsoever (such as Alaska).

- Title Company Fee- Varies according to title company but most charges between $250 to $500. Title company means the company that will handle all the paperwork and closing costs necessary to finalize a real estate transaction.

- Appraisal Repair– Appraisals cost between $300-$400 for one appraisal report so you’ll need at least two reports for your property’s net worth calculation; these fees are paid by sellers before settlement because buyers will not want to buy a property without adequate knowledge about its value. In most cases, this fee may seem like an unnecessary expense but think again! Many buyers rely on appraisals to determine how much they are willing to pay for the property.

- Title Insurance- Independence title insurance varies according to the title company, but most charges between $400-$600. This is a one-time fee paid by sellers before settlement and it covers you in case something goes wrong with the transaction like a termite infestation that isn’t disclosed or any other issues with ownership of the property. Title insurance is required in all states except Alaska where it’s optional. It protects against someone else claiming ownership of the property after you’ve purchased it or refinanced on your loan with them. The buyer pays for this upfront at the time of purchase as well as any upfront costs associated with changing titles such as deed preparation fee(s). Taxes vary by state but can average about two percent per year and sometimes additional fees based on factors such as the home value amount being sold or transferred.”

- Recording fees – $160. Recording fees are paid by buyers to record a deed for the property with either county or city offices depending on what state you live in and they vary according to location and time of year.

- Realtor commission – Listing commission is the fee that a listing agent or broker charges for services as a real estate agent. The amount may vary widely depending on location and other factors, but generally, it is between two to three percent of the home’s selling price.

- Escrow fees – Escrow is a service provided by accounting professionals or organizations that ensure funds are transferred to the appropriate party at an agreed-upon time. The money in escrow is typically for real estate transactions, where it covers property taxes and other fees from one month’s date until another.

- Closing costs – Closing costs or actual closing figures are all those expenses associated with buying or selling the property where both parties must agree to transfer ownership in some way—usually through a sale contract (purchase), deed (sale) or land purchase agreement. A seller might offer closing cost assistance if they feel confident that their asking price will be acceptable; however, this would not be considered an incentive because there would still need to be acceptance by the buyer first at which point these amounts can become part of the negotiations process. Realtor commissions are not considered closing costs.

- HOA Packets and appraisal repairs – If an HOA requires monthly dues, the seller should pay for these up until closing. These are typically non-refundable; however, a seller might offer to contribute if they feel confident that their asking price will be acceptable and would not affect negotiations.